David Solomon of Goldman Sachs recently said in an interview at the Bloomberg New Economy Forum in Singapore that we are in one of those periods when greed has far outpaced fear. The question du jour is whether there is more upside : Is ‘greed’ dominating the market or is ‘fear’ peeping to take over?

David Solomon of Goldman Sachs recently said in an interview at the Bloomberg New Economy Forum in Singapore that we are in one of those periods when greed has far outpaced fear. The question du jour is whether there is more upside : Is ‘greed’ dominating the market or is ‘fear’ peeping to take over?

I am aware that recent market chatters revolve around ‘inflation’ and why the central banks need to tighten and how interest rates would go up. But I am of the view that valuation of financial assets including venture capital will remain supported at least in the short-term. Interest rates will remain low at least in part because of higher savings. There are more savings sloshing around, exacerbated by rising income inequality: a larger and larger slice of national income is going to the top decile of earners, and these wealthy few tend to save much of this income rather than spend it, and this directly pushes rates down. If those savings are invested, it would drive up asset prices further and yields would go down. Inequality is self-perpetuating, with the feedback loop running through low rates. Excess savings of the rich depress rates; low rates push asset prices up; the rich get richer still.

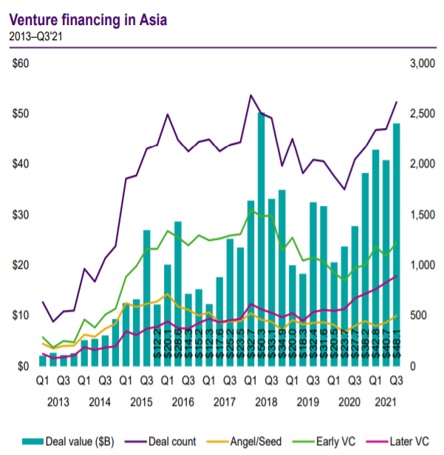

And if inflation persists, investors need to look for exposures and assets that have a better chance of outpacing inflation while also providing diversification. There is a clamour for hyper-growth companies (most of them are technology and tech-enabled) and emerging economies such as Southeast Asia. Presently investors have limited avenues to access these assets, and the politics of sentiment indicates that fear has not set in, and the economics law of supply and demand suggests there are still further upside (at least in the not too distant future).

It is worth to note that there is no physical impossibility about death, and like mortals, this exuberance may also die when the ‘fear’ snares the ‘greed’.

There is no shark like fear, there is no snare like folly and there is no torrent like greed.