I was in Jakarta this month for a short trip. Not long after arriving from Kuala Lumpur, I was almost involved in a car accident. It was partly my chauffeur’s fault; having realized that shortly after we left relatively brand-new Terminal 3 of Soekarna Hatta International Airport we were caught in standstill traffic. He performed a quick turnaround, crossing a side lane reserved for emergency use and – it turns out – mopeds, including the one that we nearly collided with. To drive in this city, you need to have your wits about you. I have survived grueling years of living and driving in London and Kuala Lumpur, and I do not think I’d ever be entirely prepared for Jakarta’s challenges. But President Joko Widodo wants to change all of that. There are several ambitious long-term plans that will hopefully survive when he leaves office in 2024. These include building superhighways, developing mass transport system, and transforming the transport infrastructure into a coherent integrated system. Although phase 1 of Jakarta Mass Rapid Transit was opened before the pandemic hit, commuters (for now) still must rely on the old-fashioned traffic police enforcement.

But on that fateful day, I saw there were police officers manning our road – perhaps the problem was none of the other drivers saw these officers (and their hand gestures)! Okay, I admit there are times and places at which it is permissible (nay, imperative) for police officers to be unrecognizable as such. No undercover sting operation would last long if the constable in the field were wearing a cap and badge. However, none of those times or places is when police officers are directing traffic. In such circumstances, it is obviously of utmost importance that the cop can instantly be identified, both to assert their authority and avoid being run over. I wonder why these traffic patrols do not embrace green- yellow high-vis after years of discharging their duties in browns or greys (or blacks and white in Malaysia) – a color scheme that almost designed to endanger those attempting to impose order on the frolicsome traffic in Jakarta (and in Kuala Lumpur). Perhaps traffic cops may not be the actual solution to our worsening road scenarios.

Could 2023 be the year that our cities finally develop and implement connected public transport and enhanced mobility using autonomous vehicle technology? Our Research team at Penjana Kapital is excited about the industry progress, and this issue is dedicated to discussing its prospect.

Self-driving vehicles and vessels – from buses and cars to ships – are finally here and big automakers and shipping companies are racing to develop fully autonomous technology. This mode of transportation will certainly be less polluting and environmentally friendly, but it will not solve the problem of congestion. Although we are fascinated by autonomous vehicles in particular their safety and when or if they will arrive en masse, the bigger and more important question we need to think about is how these autonomous vehicles (or vessels) will work with public transport to move more people with fewer vehicles to solve our urban congestion (or will work together as fleets efficiently to solve underestimated human error and pollution challenges in maritime transport).

We can never be too sure of what the future holds, but we are hoping to see shared fleets of autonomous vehicles integrated into our public transportation network. Penjana Kapital has invested in Beam, a fast-growing regional micro-mobility start-up, whose e-scooters seek to complete the first and last mile of a commuter’s journey, but this would not completely solve our urban congestion. We need to optimize the use of autonomous buses for instance by making sure that each area with users-density has the right number of autonomous (and electric!) buses to meet the local demand for transit. Essentially, these are how we can achieve and encourage more sustainable mobility, making public transportation more attractive, efficient, and equitable for more people across our cities.

The highest profile work on autonomous vehicle development is in the US and great focus is given to self-driving private cars and taxi services. Other countries are using autonomous vehicles to increase the convenience and popularity of shared transport. Spain is trialing for slow-moving self-driving minibuses for tourism in an environmentally sensitive area of the Canary Islands while Australia is testing them in retirement villages. The focus on public transport is also gradually being scaled up in Asia. Taiwan is planning to start on-road trials of autonomous buses at night to help solve driver shortage, and Singapore is rolling out driverless buses this year to expand the testing area covering public roads in the Western part of the city state of around 1,000 kilometers (one-tenth of Singapore’s total public roads).

One might have hoped that our policymakers and city planners, doubtless well-schooled in assembling conclusions from clues and well-trained in manufacturing policy blueprints from problem statements, would have figured this out sooner.

I am back from the road and in Kuala Lumpur, where my home is. And the next road is ahead. Have fun reading this issue!

“We can never be too sure of what the future holds, but we are hoping to see shared fleets of autonomous vehicles integrated into our public transportation network”

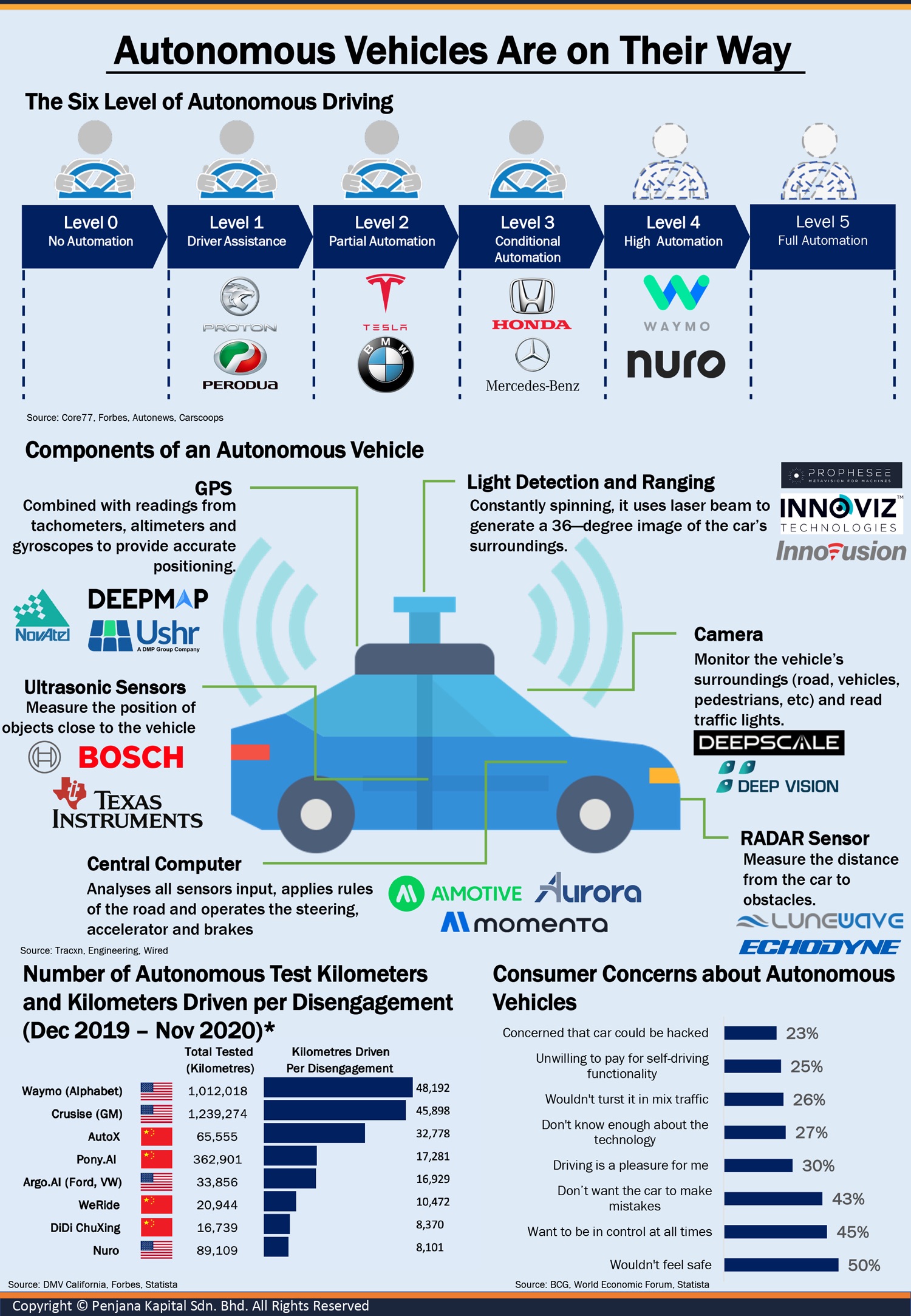

The Six Levels of Autonomous Driving

US-based SAE International is a global association comprised of more than 128,000 engineers and related technical experts in the aerospace, automotive, and commercial-vehicle industries. In 2014 they released the first iteration J3016_201401, which provides a taxonomy for motor vehicle automation. This became the foundation of J3016_202104, which is the latest version of the taxonomy with detailed definitions of the six different levels of driving automation: –

Level 0: No Driving Automation

Level 1: Driver Assistance

Level 2: Partial Driving Automation

Level 3: Conditional Driving Automation

Level 4: High Driving Automation

Level 5: Full Driving Automation

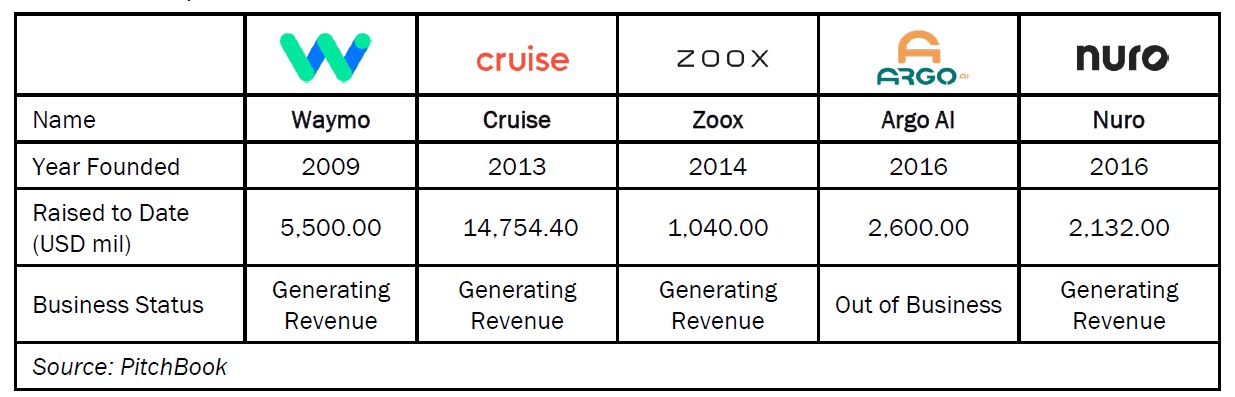

The opportunities that come with Full Driving Automation, which does not require a human being to be in the driver’s seat (and eliminates steering wheels and pedals altogether), is endless – eventually leading to the future of mobility: Transportation-as-a-service (TaaS). Gone will be the days of holding down the brakes while being stuck in traffic or spending 30 minutes looking for a parking spot at the mall, just to name a few. Driving might one day become a thing of the past, and the amount of capital that has been invested is a testament to investors’ confidence.

Last year, two of the most established players in the automotive industry, Ford and Volkswagen, even announced their decision to shut down Argo AI less than 5 years after investing in the project, as they opined that “profitable, fully autonomous vehicles at scale are a long way off”. Ford and Volkswagen had invested $1 billion and

$2.6 billion in Argo AI, respectively. The company hit a high valuation of $7.5 billion in 2020.

While the potential use cases are clear, getting to the stage of mass adoption to replace the manned vehicles we have on the roads today requires advancement in two key areas (in addition to funding): regulatory support and technological advancement.

Regulating Autonomous Vehicles in Malaysia

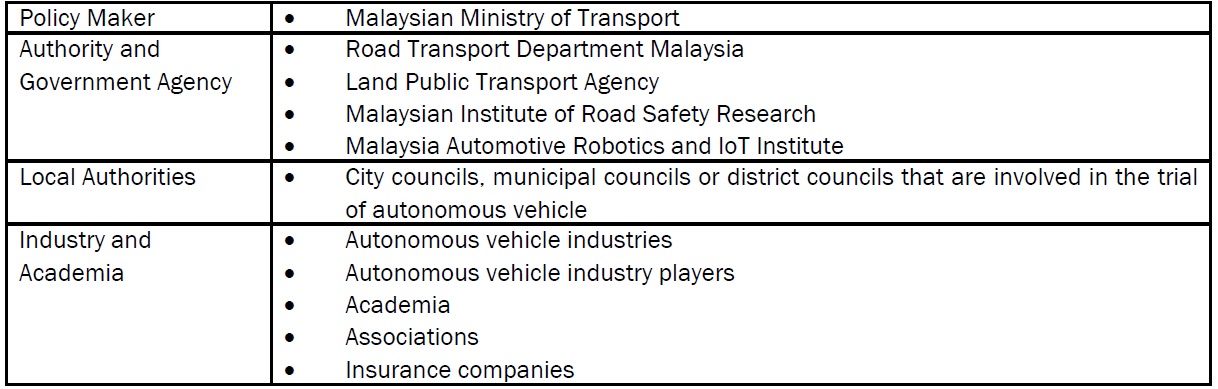

The Malaysian Ministry of International Trade and Industry recognizes autonomous vehicles as one of the key trends in the global automotive industry and highlights the need to develop Autonomous, Automated, and Connected Vehicles (AACV) as part of their National Automotive Policy 2020, which sets aims to enhance Malaysia’s automotive industry in the era of digital industrial transformation from 2020 to 2030. This shows strong intent on the government’s part to grow this vertical. Therefore, it is important to understand the key stakeholders that are driving Malaysia’s efforts to develop an autonomous vehicle ecosystem: –

In 2020, the Ministry of Transport Malaysia through the National Regulatory Sandbox with Futurise developed the first autonomous vehicle test route in Cyberjaya. In line with this, the Guideline for Public Road Trials of Autonomous Vehicle was released to set out the application processes and requirements for companies who intend to conduct trials of automated vehicles on the test routes, with the main goal of supporting autonomous vehicle technologies in Malaysia. However, only autonomous vehicles up to Level 3 are allowed for now.

Malaysian start-up eMoovit Technology Sdn Bhd was then announced as the first company to receive approval to use the routes to test its autonomous vehicles on the test route. This initiative is important to allow for the testing of both software and hardware developed for autonomous driving in a safe and controlled environment, which allows substantial data collection and monitoring for future product improvements.

Challenges to Overcome

When it comes to any novel technology, there are bound to be barriers to be overcome before it can be adopted on a massive scale. And when it comes to autonomous driving, there are many erratic variables that are still hindering progress – autonomous vehicles hate unpredictability, and driving in Malaysia is full of it.

According to a study conducted by Zutobi, Malaysia has the 12th worst roads in the world, and even has the second highest number of road deaths at 22.76 per 100,000 people (for comparison, Singapore’s is 1.69 per 100,000). Poor road infrastructure quality can be very hazardous in the case where the lidar sensors in autonomous vehicles fail to detect potholes or sizeable debris in time, especially when going at high speeds.

Besides, other unwelcomed variables such as illegal roadside parking and construction barriers, which are very ubiquitous in Malaysia, can also surprise any autonomous vehicle software and thereby still require human intervention. Of course, the hope is that all the billions of dollars in investment plowed into research and development will improve autonomous vehicles up to the point where these vehicles are able to deal with these, making Level 5 commonplace one day.

But if we were to encapsulate every obstacle into two key issues, it would easily be (1) road safety and (2) liability protection. While issue #1 can be somewhat mitigated by further product refinement, #2 is especially tricky – who bears the responsibility in the case of an accident caused by an autonomous vehicle? Would the vehicle owner who is responsible for manning the vehicle be liable or would the car company that rolled out dangerous technology be liable? Judging by Kevin George Aziz Riad’s ongoing court case, the onus is still very much on the driver to pay full attention on the road.

Tesla’s (and the autonomous driving industry’s) arduous journey towards mass adoption of Level 5 could very well be an expensive, long journey ahead.

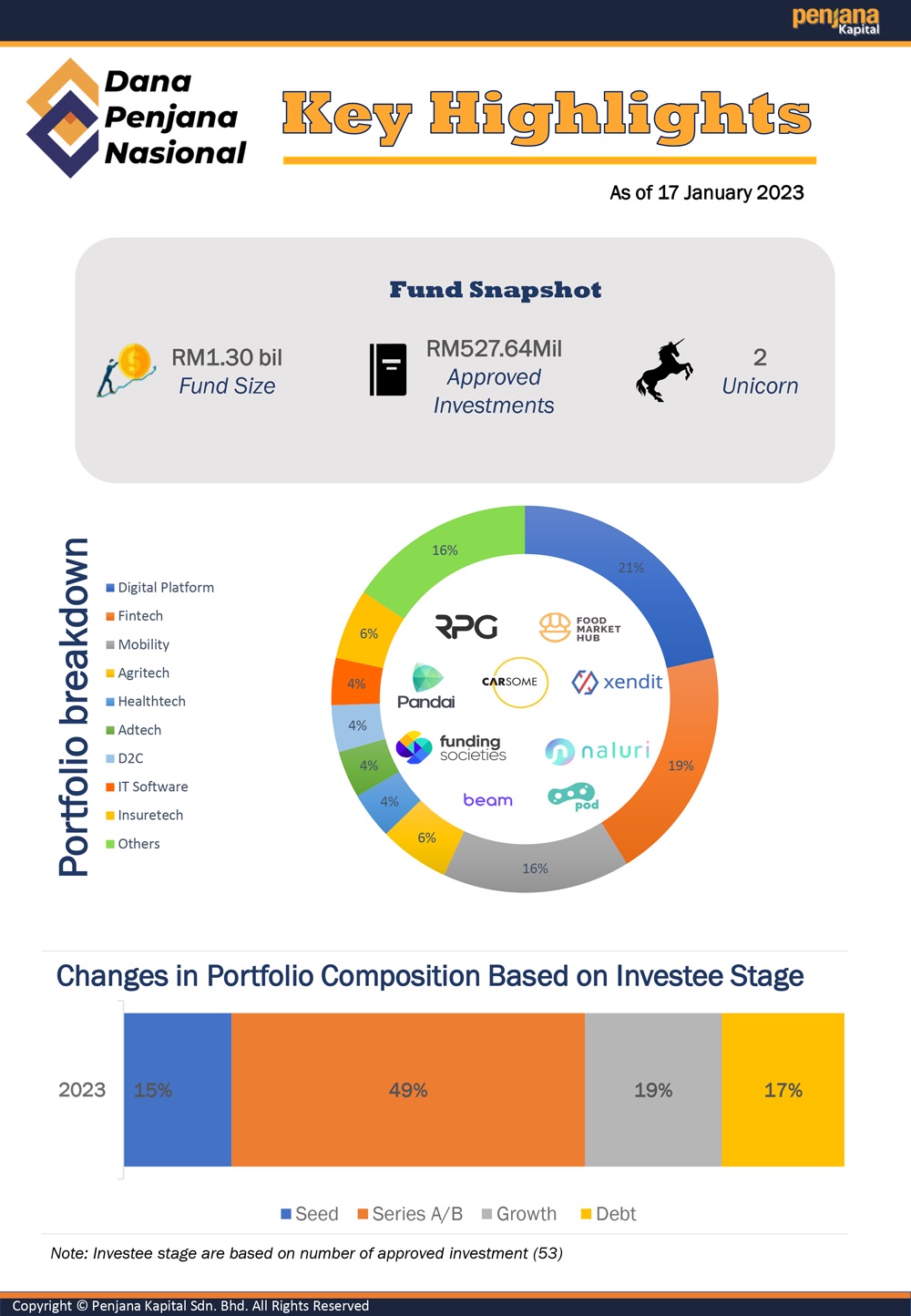

On 17 January 2023, MDEC, Khazanah and TalentCorp held a Malaysia Digital and Tech Talent Roundtable discussion with industry players including local government ministries, government agencies, investors, venture capitalists, corporates, start-ups as well as public universities to understand current issues and generate ideas to spur digital-ready talent for Malaysia.

Our CEO, Taufiq Iskandar was invited to give the closing remarks at the end of the roundtable session. The speech is transcribed below:

Digital Talent Workshop (closing remarks)

Good afternoon distinguished guests and friends. Congratulations on the conclusion of today’s workshop. We have often heard about the bright economic prospects of Southeast Asia as a whole and the challenges facing the region, and Malaysia needs to respond to these challenges to remain economically relevant in the region. My job is to do the closing. Unfortunately, I think the mood is much more somber when we talk about talent. There are gathering storm clouds of possible civilizational conflict between an aging Pax Americana and a rising Pax Chinica. Even though the proverbial thunderstorm has not yet burst forth however we do face the prospect of the gray chilling and unceasing drizzle of another ‘Cold War’ especially after the military aggression in Ukraine- Russian border, which could spread to Chinese Strait as well as Korean Strait and in the Peninsular.

Today I want to talk about another war, and that is a war for talent especially digital talents. There is no playbook for managing this fundamental tension to satisfy countries and civilizational needs for capital. The former, conventional conflict is largely a political-economic issue as countries redefine land-sea border and search for natural capital. The talent war is about socio-economic, and it is about human capital i.e., another key economic factor of production. Though Digitalization offers greater opportunities ahead, it also means diminishment of physical borders where talent movements flow easily. No one can possibly forecast today where we will be in five years or where we will be at the same time next year. But today I want to highlight two broad dynamics that, in my view, perhaps be apparent in the future months ahead.

First, de-globalization, though I would prefer to say the rise of self-sufficient economies. We have heard “Make America Great Again” in the west and “Make China Great Again” in the east. The search for self-sufficiency is driven by the need for countries to have strategic autonomy over supply chain and more importantly key resources – from natural resources to human and financial capital! Our geographic physical world is increasingly more polarized as a result.

Second, our digital world is bifurcated. And this represents another setback for countries such as Malaysia to realize its economic potential. We have seen decoupling much of the digital universe with for example WeChat and Weibo versus WhatsApp and Twitter, between Huawei Kirin chips and Nvidia chips. A more extensive digital decoupling can be seen in digital infrastructure and technological advancement. We have seen how developed countries accelerate the development of their IT infrastructure on the back of wider digital adoption whilst most of the world is lagging and still grappling with poor internet access. The economic and technological inefficiency slows down growth.

Even in Malaysia, we have seen a disparity in terms of digital infrastructure readiness between Klang Valley and the rest of the country. This means opportunities are not evenly distributed. Though talent may be everywhere, opportunity is not. We will lose out if we do not create opportunities quickly. Bright talents congregate around opportunities.

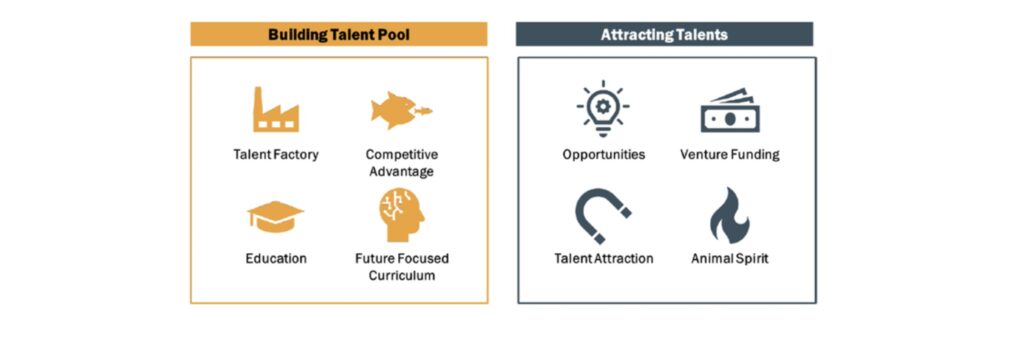

In a physically more polarized world, we need to make Malaysia a talent factory. Like a production factory, the system must be built on future-ready design, is run collectively and continuously, machined to specified standard, and utilized massive amounts of aggregated data to adapt to increasing variability.

Let’s take Silicon Valley as a case in point. Even though it does not rely on natural resources and is not a port city or a connecting hub – unlike Malaysia who is blessed with natural capital and competitive advantage, it relies on its ability to both create and ride the technological wave of the future to grow into the innovation powerhouse it is today. It does this primarily by realizing the power of the internet and developing the software economy that is needed to power it.

Almost all Silicon Valley tech giants do this. Even Tesla, the electric carmaker, is a software-focused company, whose cars are referred to as ‘smartphones on wheels’. For Malaysia to have its own Silicon Valley, we need to harness our blockchain technology and artificial intelligence capabilities. These are two major technological waves of the future. We should and we can.

To realize this, we need to set up a future-focused curriculum. Silicon Valley has Stanford University, San Jose and UC Berkeley to name a few, and these institutions are the intellectual power batteries that drive the Valley. They have had a decades-long focus on engineering and computer science, which has birthed some of the best technologists the world has seen, who have gone on to produce the innovations coming out of the conveniently proximal Silicon Valley companies. To emulate this, select public universities in Malaysia should institute a future-focused curriculum that concentrates on developing and building upon the future technologies, which would invariably include both artificial intelligence and blockchain technology. If we are to become leaders in these budding technologies, it is about time we started integrating them into our education curriculum, the earlier the better.

But we must admit its limitation. We are a country of 33 million people. Even if we develop and retain all our talents, it is not enough. We need to attract new talent. In a digital world, there is no such things as Malaysians, Singaporeans or Indonesians: we are all netizens where talents move beyond borders. We must then make Malaysia a land of opportunities. When it comes to attracting talent, it is all about opportunities.

One of the biggest grievances I have heard about Malaysia since I returned from London is the lack of venture funding and ‘animal spirit’. Money is the lifeblood that drives entrepreneurship and allows entrepreneurs and innovators to take the risks necessary to create potential disruptive inventions. Without a healthy amount of financial capital (especially smart money) flowing into the ecosystem, these passionate entrepreneurs will flounder, and bright talents will not migrate to Malaysia. Like power, talent tends to concentrate. It is what we call a Pareto Principle. Talents will migrate to a more nurturing market, where opportunities are concentrated. This is an area that sets Silicon Valley apart from other technology hubs. Its venture capital ecosystem is second to none. This is also an area that South Korea and Singapore focus on. These countries leverage on their venture money to attract promising start-up entrepreneurs to relocate and entice highly skilled talents to migrate. Penjana Kapital was established to make our local venture landscape more robust and vibrant. But we cannot do this alone. We are all in the same boat together. Thank you.

KapitalX Cohort 1 Graduation Ceremony – Class of 2022

The inaugural KapitalX programme, Malaysia’s first Junior Venture Capital (“VC”) talent development programme, concluded on 23 November 2022. 32 participants have successfully graduated from the programme upon undergoing a 5-week classroom training and a 1-month venture fellowship with 14 VC firms.

The KapitalX programme is Penjana Kapital’s flagship talent development programme established to develop venture capital talents with the competencies to be world-class investors. Launched in April 2022, KapitalX gathered a cohort of university students in their penultimate year, recent graduates with less than two years of experience and entrepreneurs or early-stage start-up employees.

Please look out for two new programmes – Cohort 1 of the VC senior management track and Cohort 2 of KapitalX junior track in 2023. If you are interested to join the new programmes, please fill up this interest form https://bit.ly/3EP2LgT

| DISCLOSURES AND DISCLAIMER |

This Newsletter is strictly informational and is issued Penjana Kapital Sdn Bhd (“PKSB”) on the basis that it is only for the information of the particular person to whom it was provided. This document may not be copied, reproduced, distributed or published by any recipient for any purpose unless Penjana Kapital Sdn Bhd’s prior written consent is obtained. This newsletter has been prepared for information purposes only and is not intended as an offer to sell or a solicitation to buy any securities, and/or any other product in Public or Private markets. Penjana Kapital Sdn Bhd is not making any recommendation to buy any securities or other product and the information provided should not be taken as investment advice.

It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Penjana Kapital Sdn Bhd has no obligation to update its opinion or the information in this newsletter and Penjana Kapital Sdn Bhd recommends that you independently evaluate particular investments and strategies and seek the advice of a financial adviser prior to entering into any transaction. The appropriateness of a particular investment or strategy will depend on your individual circumstances and objectives. The information herein was obtained or derived from sources that Penjana Kapital Sdn Bhd believes are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. All opinions and estimates included in this newsletter constitute our views as of this date and are subject to change without notice.

Penjana Kapital Sdn Bhd is not acting as your advisor and does not owe any fiduciary duties to you in connection with this newsletter and no reliance may be placed on Penjana Kapital Sdn Bhd for advice or recommendations of any sort. Nothing in this newsletter shall constitute legal, accounting or tax advice, or a representation that any transaction or investment is appropriate for you taking into account your investment objectives, financial situation and particular needs, or otherwise constitutes any such advice to you. Penjana Kapital Sdn Bhd makes no representations or warranties, express or implied, with respect to the accuracy of the information or fitness for any particular purpose and does not accept any liability (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) for any use you or your advisors make of the contents of this newsletter or for any loss that may arise from the use of this newsletter or reliance by any person upon such information or opinions provided in the newsletter. This newsletter has been prepared by the analysts of Penjana Kapital Sdn Bhd. Facts and views presented in this newsletter may not reflect the views of or information known to other business units within Penjana Kapital Sdn Bhd. This information herein is not intended to constitute “research” as it is defined by applicable laws. This newsletter is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information provided in this document has been obtained or derived from sources believed to be reliable. Penjana Kapital Sdn Bhd does not guarantee its accuracy or completeness and does not assume any liability for any loss that may result from the reliance by any person upon any such information or opinion. Such information or opinions are subject to change without notice, are for general information only and is not intended as an offer to sell or a recommendation/ solicitation to buy any securities, foreign exchange or other product.