On Wednesday, just before 2am in San Francisco, my phone started pinging with news notifications. I looked at the screen: Asian stock markets fell sharply with Chinese Technology companies suffered heavy losses. I lay there in the dark, unease spreading with every update. I was in Palo Alto to meet Accel, Goodwater Capital and other venture capital firms as well as Y Combinator a day before. I was using the time difference to gauge how the US markets would behave once the opening bell is rung. I could not sleep. And then the day barrelled on. The Dow Jones Industrial Average dropped 1,100 points for its biggest decline since 2020, the S&P500 and the Nasdaq shed over 4%. Across that Wednesday, as markets suffered heavy selling, investors and traders wondered if rising inflation would take a bite out of consumer pockets and corporate profits.

Imbibing too much rolling news could often make you feel as though you might lose your footing. But my response was more than news anxiety. This is not going to be some painful market loss. No, this is a reminder that, as we are quickly realising, resets the economic expectation. As inflation accelerates, economic outlook dims.

In the evening, I went for a meal with close acquaintance and his friend who is also a partner at Accel. Do you think it would be possible for economy to fall into a recession I asked? They answered, without hesitation, that it is possible, and the next downturn is likely to be consumer recession. Although consumption has held up well this year, the persistent inflation will eventually sap consumer sentiment and spending. The three of us agreed that potential slowdown will be shallow and short though we are not ruling out it may worsen if inflation and inequality become deeply entrenched.

As I was heading west that weekend, the world leaders descend upon Davos for World Economic Forum 2022. Davos throws up wardrobe challenges and the Forum serves as a platform for intellectual discourse to offer solutions for a better state of the world we live in.

I used the spare time I had in the plane to think (Personal Fact: I am terrible at sleeping on planes). I travelled back in time.

The Global Financial Crisis 2008 marked as a turning point that shook virtually every country, government and household and it gave way to a “new normal” of low growth, rising inequality, political dysfunction, and in some cases, social tensions despite massive monetary policy interventions. Sensing that elected policymakers were paralysed by excessive politicking, central banks then found experimental ways to keep the economy on a growth path, and they did so even though the underlying engines of economic prosperity were yet to be revamped. Recently the world was shocked by the devastating spread of Covid-19. The pandemic too was a historical inflection point – unthinkable became more common, and insecurities became more prevalent. Acknowledging that central banks’ ability to repeatedly pull new rabbits out of their policy hats has been stretched, government across the world stepped in with massive fiscal supports.

Yes, policymakers managed to arrest the spread of horrendous financial crisis and economic calamity, and thus averted tremendous human suffering. For all that, we should be grateful for their creativity and courage. As hard as they had tried, I wonder whether they have firmly placed our economy on a sustainable path of high inclusive growth and durable financial stability.

Our economy is still saddled with key issues whose detrimental consequences are multifaceted and worrisomely self-feeding. Our prolonged reliance on money-printing/giving policies will be outweighed by collateral damage and unintended consequences. The concerns are not limited to price formation and inflationary surge. They extend well beyond to issues of inequality and growth imbalances.

Fuelled by an unusual combination of cyclical, secular and structural factors, the worsening of income and wealth inequality has been pronounced that it now also undermines opportunities, giving rise to what some call “inequality trifecta”. Worsening inequality is not new. It has been a feature of several countries – Malaysia is no exception.

The expansion of central banks’ balance sheet has tended to support the wealthy since the latter hold a disproportionately large share of the financial assets that benefit from those supports. Meanwhile, active budget policy and transfer payments as well as subsidies for the poor are heavily constrained by political polarisation. The persistent trust deficit and loss of institutional credibility further undermine the legitimate redistributive function of government. In addition, the changing nature of technological advances favours higher-skill individuals and those risk-taking entrepreneurs. In relation to opportunity, the emerging evidence of youth unemployment to health and educational attainment is also concerning. The greater the inequality, the larger the access gap to education opportunities as well as socio-wellbeing: both important determinants of employment and earning prospects as well as entrepreneurial capacity. Family circumstances have been playing a larger role in determining the income and wealth configuration of the next generation.

Low-income households are hit hardest by inflation: it erodes their real income, weakens their purchasing power as well as corrodes the value of their savings and financial capacity, potentially limits future opportunities.

This month’s issue of The Kapitalist explores the impacts inflation has on consumers and consumer-facing start-ups.

We have taken the precaution and assure that the content is not distressing so that our readers are having fun reading it!

“Inflation” seems to be the buzzword in recent months following the tremendous market exuberance arising from record-breaking quantitative easing (QE) and expansionary fiscal policy to support economies all over the world. While inflation typically is a sign of strong economic growth, the growing concerns on inflation spiralling out of hand is not without reason. Inflation, if left unattended, could build on itself and diminish the real value of money and purchasing power especially if wage growth and real wealth fail to keep up. When purchasing power diminishes, consumers must expend time and effort to minimise the effect of inflation on their finances, otherwise known as “Shoe-leather Cost”.

Businesses, similarly, are affected by inflation. For instance, business will incur more costs and have no choice but to raise prices to survive. Raising prices would then require a host of internal changes, leading to “Menu Costs”. Salaries and/or wages, a major component of fixed cost, tend to be sticky-down and would often lag in times of inflation as business take a prudent stance to manage bloating costs, contributing to loss of consumer purchasing power.

Of course, they are many other reasons why inflation needs to be contained but for the sake of brevity, let’s move on.

Cost Push, Demand Pull

The inflation we are experiencing is unique because it is not only due to higher money supply and aggregate demand thanks to the excessive QE and fiscal support but is also largely due to the shock to aggregate supply which also creates higher costs i.e., “Cost Push inflation”. Labour shortages owing to Covid-19 containment measures, severe drought in South America, and geopolitical tensions all contributed to higher commodity prices and supply chain disruptions. This has all contributed to inflation in a highly globalised economy like today.

Unlike Demand Pull inflation, the current Cost Push inflation we are seeing is trickier to solve. There needs to be long-term structural changes that solve long-standing issues such as supply chain inefficiencies, food insecurity and climate change to manage supply. Besides, there are other problems other than spiralling inflation that could be brought upon by these issues – population growth, famine, malnutrition just to name a few.

Food inflation and food insecurity are concerning by-products of the current macro trend. While the government has taken protective measures to maintain affordability such as price ceilings, it still does not solve the issue of global food supply. Malaysia, a net importer of food, still depends largely on global trade for constant food supply, creating dependency risk. There has been serious concerns on global food supply due to shortages of water, land, and energy combined with the increased demand from population and economic growth.

There must be measures to ensure ample global supply of food. The trend of higher food prices, a burden consumers are feeling now, will effectively reduce consumer purchasing power and shrink overall consumption basket in the case where income growth falls behind due to it being sticky-down.

A Balancing Act

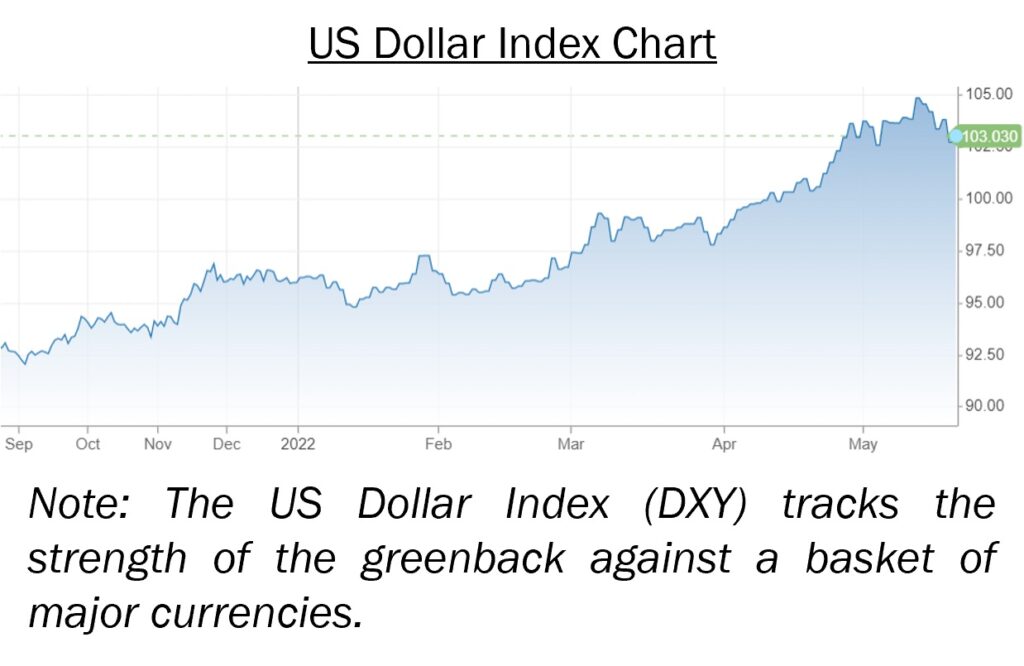

In a bid to curb inflation, Bank Negara Malaysia recently announced a 25-basis points hike to the overnight policy rate, following the footsteps of the US, Malaysia’s third largest trading partner. This move could be seen as both reactive and proactive: reactive to the hike in the federal funds rate in view of the strengthening US Dollar, and proactive in managing inflation in view of the reopening of economy and improving labour conditions. Unemployment, for instance, is on a downward trend while labour participation is improving, signalling strong market recovery.

Nonetheless, managing inflation is a delicate balancing act, and is not without implications. A higher interest rate environment lowers demand for high-risk assets, hampering growth expectations. Companies start to conserve cash and cut costs as capital becomes more expensive and tapping the capital market becomes a challenge due to higher required rate of return from investors and lenders alike.

The bull-run seems to have taken a drastic U-turn.

Financial Wellbeing

As the saying goes, sediakan payung sebelum hujan. The rate hike is a move in the right direction. However, inflation, especially Cost Push inflation, does not look like it is going away anytime soon – there is only so much monetary and fiscal policies could do to manage Cost Push inflation. The signs of an overheated global economy is ubiquitous, and a correction is due. It will be a bumpy ride until the economy (and inflation) returns to normalcy as that really hinges on a variety of factors.

The current economic climate has reinforced the need for better financial planning. The only way to maintain purchasing power in highly inflationary market is to simply outrun inflation. Investments, income growth, and savings are key to grow real wealth, but it is still exceptionally challenging when inflation eats up into any appreciation of wealth.

Fortunately, start-ups like Pod and Payd were founded with the goal of better financial inclusion and wellbeing. Pod is a micro-saving app that enables users to slowly build their savings towards their desired goals, effectively track expenses while earning lucrative rewards. As for Payd, it alleviates financial stress by allowing users to access up to 50% of their earned salary, which enables better budgeting and eliminates the need for the needy to utilise payday loans and loan sharks which can create even greater financial burden. Start-ups like Pod and Payd are solving real-world bread-and-butter issues, and their utility is much needed especially in the current economic climate. The solution to erosion of real income starts with the perseverance to grow household wealth.

Winter is Coming

In the past week (mid-May as time of writing), the start-up and venture capital (VC) community were buzzing on a particular letter written by Y Combinator to advise its portfolio companies to brace for the impact ahead on social media.

Unsurprisingly, this comes after the expected interest hike by the US Federal Reserve Board. The interest hike did not catch the public markets by surprise. It was inevitable as the US continues to battle sky-rocketing inflation, amongst other factors such as geopolitical tension and supply chain issues.

Why is this warning significant?

For context, tech stocks have not been performing well as of late. In fact, as reported by Wall Street Journal in April, the Nasdaq is down 21% in 2022. This is the worst start to a year on record. This decline of tech stocks mark a dramatic shift from recent years where tech companies have been one of the biggest benefactors of the pandemic-driven QE and fiscal support.

Additionally, TechCrunch reported that big tech giants are feeling the pressure to cut down on their operating expenses amid rising interest rates and a looming bear market. Netflix laid off 150 employees in May amid stalled growth, a month after laying off its staff at its fan website arm, Tudum. TechCrunch also reported Meta, Robinhood, Salesforce and Uber all had initiated hiring freezes or layoffs as well.

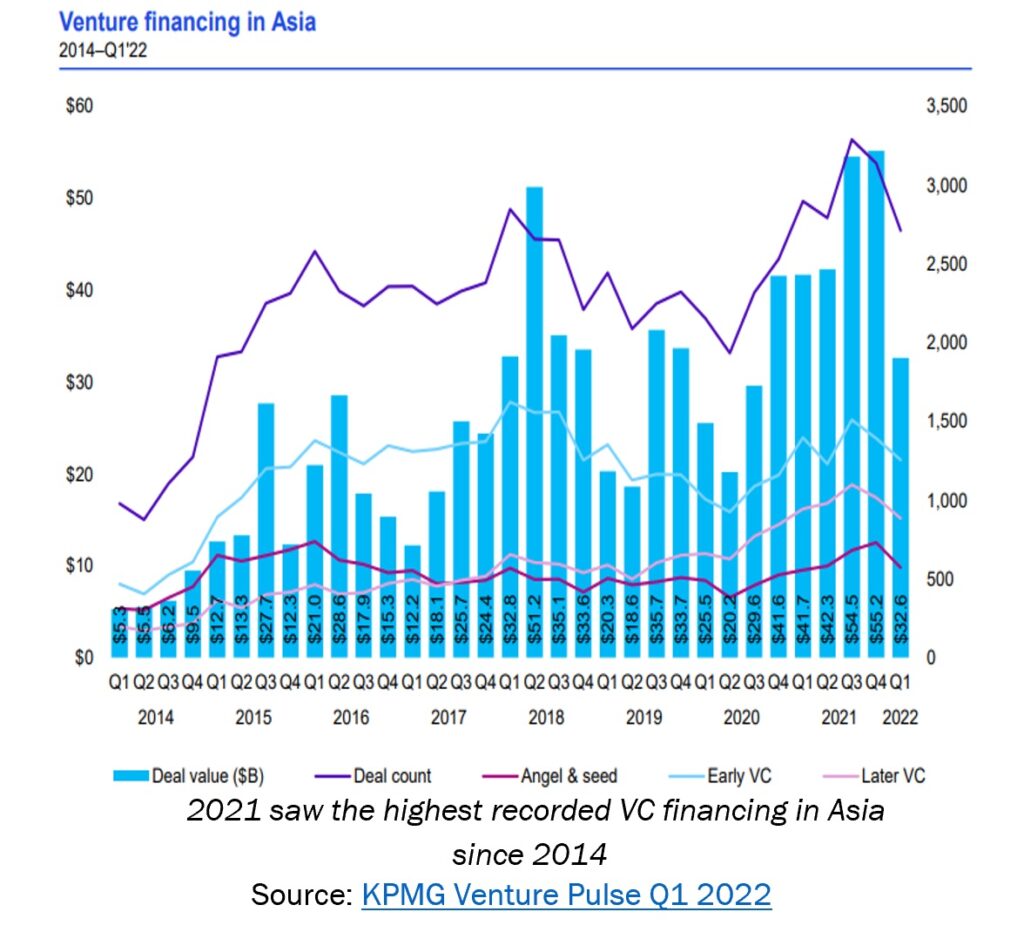

Globally, KPMG reported that Q1’22 had shown a slowdown in IPO activity as capital markets experience significant volatility in the wake of the Russia-Ukraine war. All major capital markets were affected by stock market volatility leading to tech start-ups reconsidering their plans for a 2022 IPO exit. Pressure on valuations may lead to start-ups halting their fundraising soon in hopes that the valuations will bounce back to the heightened valuations seen in 2021.

Bracing for Impact

The next half of 2022 will impose more challenges amid rising inflation, further interest hikes and market volatilities that will affect markets globally. Echoing Y Combinator’s sentiment in their letter, poor public market performance of tech companies significantly impacts VC investing. In 2021, we have seen record highs in terms of VC financing globally coupled with extraordinary high valuations for start-ups.

In contrast, the remainder of 2022 may not be as rosy as the past year. VCs tend to become more cautious during an economic downturn. Due to this, start-ups would likely face lower valuations and raise smaller fundraising rounds.

Start-ups who have shorter runways, high cash burn and are asset heavy may find themselves in a tough situation during an economic downturn. Customer spending and consumption may be less, and operating costs may spike due to higher cost of doing business. That said, huge opportunities can be found in economic downturns for founders who are adaptable, plan and strategise well.

Similarly, investors would find many opportunities during an economic downturn. Whilst there may be a slowdown in terms of deployment, this does not mean a complete absence of capital. High quality companies with real viable business models will continue to get funded. IPO exits would also be likely, although the volume and valuations may be less significant.

Nonetheless, there may well be a silver lining. As start-ups try to manage cash burn and cut operating expenditures, there could be contraction in the job market. High quality founders with ambitious aspirations might take the plunge and start their own companies – a few of which could possibly be hidden gems in the making. After all, some of the best companies in history such as Microsoft, Facebook, Airbnb, Google and Uber were founded during challenging periods.

High inflationary pressures prompted the Fed to raise interest rates. Be that as it may, the Fed is still behind the curve in terms of raising rates to cool down the economy. They are expected to raise rates at a steeper pace (Fed just hiked 0.75 percentage point recently – highest in years).

Inflationary pressures, coupled with stagnant wealth/income appreciation, have led to many people globally feeling like they are stuck because their savings are running low and their cost of living is running higher. This results in a slowdown or potentially a sharp drop in the general economic activity, which in turn could limit wage growth and cause job losses even if prices remain high. Whilst the world has now come out of battling the COVID-19 pandemic, there is a new fight on the horizon – in the form of high inflation. Governments all over the world and its central banks are trying to solve this by inflicting some economic pain (in the form of higher interest rates) to alleviate the problem.

It felt like it was just yesterday when the “Great Resignation” was rolling at record rates around the world. Both the number of employees leaving and rate of hiring across the board were soaring. This is mainly fuelled by a wave of new jobs on the back of a strong labour market offering ample amount of job opportunities.

The Great Layoff is in Session

Most corporates, notably, tech corporates have started to feel the heat from rising business costs from high inflation. Tech giants Meta (formerly known as Facebook) and Twitter had recently announced publicly that they are on a hiring freeze while PayPal, the payment giant, has let go dozens of employees. Moreover, Tesla, which has over 100,000 employees globally, is reportedly planning to cut down 10% of its staff after CEO Elon Musk expressed that he has a “super bad feeling” about the economy on Twitter.

With rising interest rates, cost of capital becomes more expensive. Start-ups are finding it hard to raise money from investors, as investors are seeing a gloomy sky in the short to medium term. This has forced start-ups to rethink their cost structure. In the past two months alone, we have seen start-ups such as StashAway and iPrice laying off 14% and 20% of their staff strength respectively and Kaodim going under. Even e-commerce giant Shoppe had recently announced they are laying off half of their headcount in Thailand and will be ceasing its operations in France and its early-stage pilot in Spain.

To sum it up, a total of 137,919 employees and out of that 35,000 workers from tech companies globally have been laid off according to Layoffs.fyi. Whilst these numbers look worrying, there is another side to the coin. There are currently 35,000 talents who have built tech start-ups and corporate tech business units available in the labour market globally. With recent tech talent shortage and general economic activity picking up pace in other parts of the world, we can see many talents joining ranks of start-ups or corporates who have a strong balance sheet and are “gung-ho” on achieving exponential business growth.

The Heat Catches on in Malaysia

Malaysia is not excluded from the global rise in inflation. The Department of Statistics of Malaysia (DOSM) had just announced that food inflation in Malaysia had risen to 5.2% in May 2022, the highest since November 2011. This announcement does not come as a surprise as most Malaysian consumers have felt their purchasing power shrink recently as evidenced by multiple viral posts. Recalling to our last newsletter, naturally, the shrinking purchasing power and erosion of real income is a cause for concern. Perhaps one of the obvious ways to combat this is through earning more income and to do this, one has to secure better employment opportunities. In this economy, this seems to be a tough feat especially with “The Great Layoffs” happening as we speak.

Before we delve further on this topic, perhaps it is best to provide context on the labour market in Malaysia. According to DOSM, there are over 15 million employed persons in Malaysia in 2021. Out of this, 78.5% are employees whilst 3.4% are employers. 64.9% of the workforce in Malaysia are in the services industry followed by 16.6% in manufacturing and 10.3% in agriculture.

Naluri is a wellness healthcare app focused on preventive and treating chronic disease by focusing on mental and physical health. The company designs, develops, and offers health technology solutions that apply AI and machine learning, and combines data science with digital design, to achieve breakthroughs in digital diagnosis and intervention therapies for chronic disease.

A fintech company specialising in payment infrastructure for electronic point-of-sale with the option to process and accept debit/credit card transactions, and core infrastructure for banking as a service.

Alternative battery solutions for advanced electric vehicles. Log9 is India’s leading nano-technology company with established cutting-edge expertise in the world of materials i.e., Graphene. It is incubated at the “TIDES Incubation Center” of IIT Roorkee from 2015-2017. They have filed for more than 26 global patents and are focused on the electrification of commercial vehicles ranging from 2-wheelers, 3-wheelers to lower calorific value and higher calorific value vehicles. Their 3 key technologies are (i) rapid charging batteries, (ii) Graphene-based supercapacitors and (iii) Aluminium fuel cell.

Accendo is a Software-as-a-Service (Saas) talent intelligence platform. The company helps organisations build talent pipelines to align with their business needs by bringing a data driven approach to talent management and managing invisible leakages in the organization.

A platform that provides instant access for workers to receive their paycheck in advance – also known as Earned Wage Access. Whilst this can benefit all core sectors of Edgenta, Healthcare may still be the biggest winner should there be collaboration between Payd and Edgenta.

Targeting the B40 segment, Payd may assist the less fortunate patients by advancing their paycheck to pay for their medical bill.

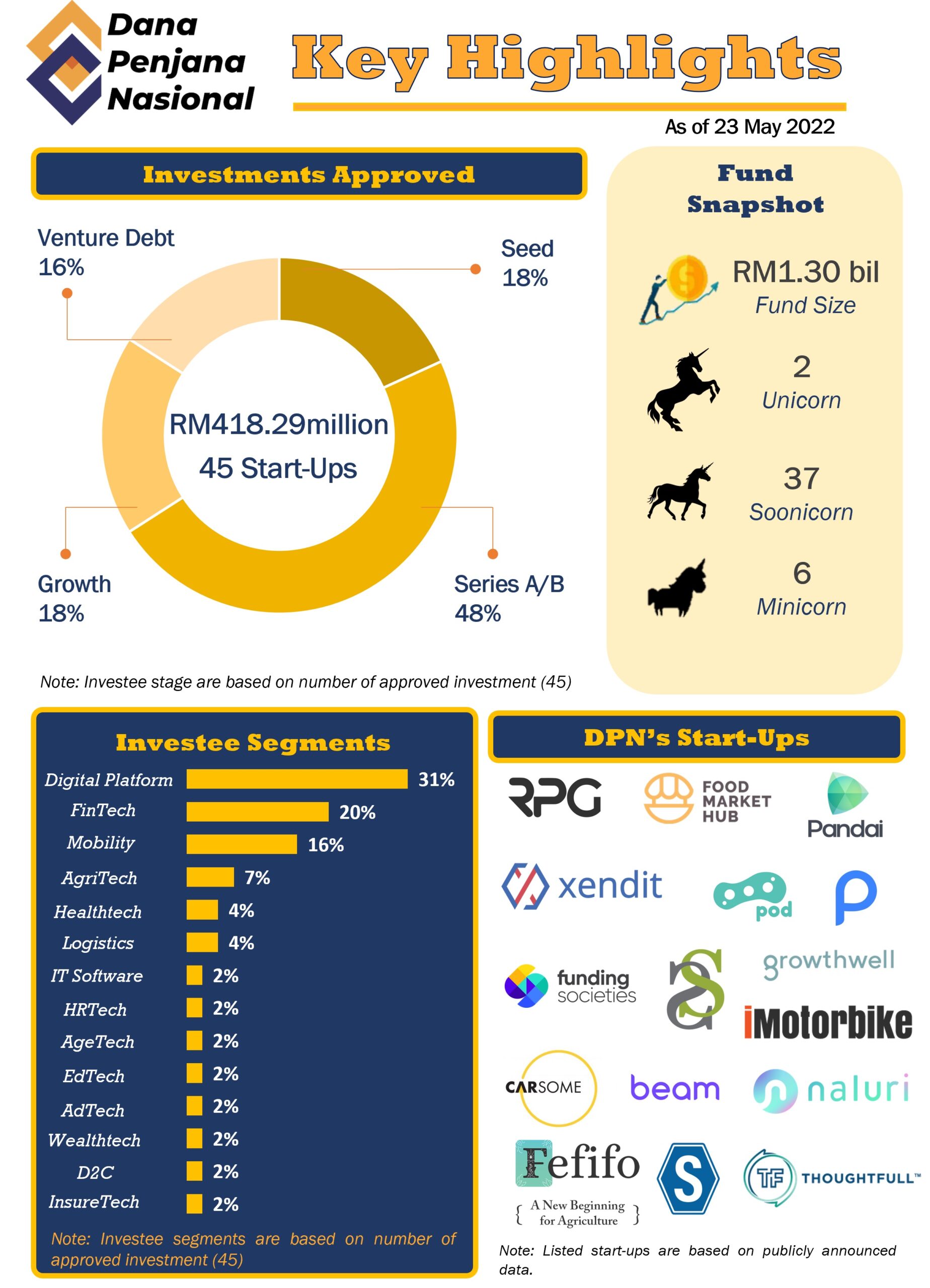

This month edition’s Start-up of the Month features Soft Space, a leading fintech player. We interviewed Chris Leong, Chief Strategy Officer to better understand Soft Space’s current and future aspirations, as well as the challenges that he foresees start-ups could face in the current economic climate.

Soft Space is an investee company under Penjana Kapital’s Dana Penjana Nasional programme via Hibiscus Fund LP managed by RHL Ventures and Korea’s KB Investment.

1. Please tell us about yourself.

I am Chris Leong, the Chief Strategy Officer of Soft Space. My role involves providing strategic oversight to ensure Soft Space remains as a competitive fintech player in the market. I am also involved in strategic partnership and capital fund raising for the company, which enabled Soft Space to complete three rounds of funding with our Japanese investors.

Joining Soft Space since its inception in 2012, I have witnessed the company grow to become one of the fastest growing fintech company in Asia Pacific. In April 2020, we were recognised by IDC Financial Insight as one of the fastest growing fintech companies in Asia, having to serve over 24 financial institutions across 10 countries today. While our clients are traditionally financial institutions (FIs), we also work closely with top tech companies and start-ups, one of them being a unicorn in Europe and another in the Philippines.

2. What is Soft Space about?

We came to being in 2012 with a mission to make payments as frictionless as possible and to reshape the traditional payment landscape. We don’t provide solutions directly to consumers but instead work with other companies such as FIs to make it easy for them to get micro and small business onboard the digital payment train via our mobile Point-of-Sale (MPOS) products, which are cost effective, easy-to-use, secure and that meets all regulatory compliances.

We still work this way today and our products still adhere to the aforementioned philosophy, but our clientele has expanded beyond FIs to include any businesses that want to offer payments on top of their core products. Essentially, we offer fintech infrastructure services under the fintech-as-a-service (FaaS) model, which simplifies the complexities of financial infrastructure and provide value-add to our customers for them to grow their business, including banks and corporate companies globally.

Our FaaS model extends to two major areas: One is to offer white label e-wallet solutions, which means that our clients, which do not have the payments expertise, to offer payment services and even issue payment cards to their customers. The second area is to promote contactless payment acceptance through our flagship product, Tap-on-Phone known as “Fasstap.” Fasstap transforms any Android devices with near-field communications (NFC) and enable them to accept contactless cards, and this technology is trusted by largest payments company in the world. Put simply, a business can just download our app onto an NFC-enabled device, perform know-your-customer process and provision the app to start taking payments in mere minutes.

With Fasstap, the potential for payment acceptance is huge as there are up to 2 billion devices and more than 180 million micro and small merchants can benefit from using this tech worldwide, according to Visa’s estimates. Soft Space has already introduced this technology to 26 partners globally, some of which are unicorn payment giants that have the most stringent business and security requirements. This validation is a great milestone for us, and we are proud to bring a Malaysian-made technology to some of the best and largest companies in the world and this is how we are further democratising payments.

3. How is Soft Space reshaping finance?

Our mantra is to “Reshape Finance,” and thus we are constantly evolving and thinking about how to meet the needs of our customers. Over the 10 years of our existence, we have amassed the expertise to build a core technology platform that allows us to pivot away from merely creating standalone products to become FaaS provider. Just like how a business consumes electricity, water or software over the Internet, we as a FaaS provider can provide fintech services to our customers using a service consumption model and that FIs would only need pay according to their usage demand. This helps FIs save costs as they do not need to invest in developing high quality fintech services that are highly secured and that meets international standards. It also helps them reduce the need to manage the complexity of navigating the new era of fintech including dealing with cyber security and regulation.

For example, we can empower a healthcare provider or a shopping mall offering finance options for its patients and shoppers respectively. These companies’ core expertise (healthcare and retail) will complement their core services with financial services and offered in a holistic way to their customers. This is where we see the opportunities for us to expand our client base by tapping into many other sectors with endless possibilities – and this is how we’re reshaping finance.

4. How are you preparing for rising inflation and economic downturn?

We have benefited from having our base strategically located in Malaysia, where the cost of tech talent is more attractive compared to other developed markets. Thus, we can maintain a competitive cost structure while serving our global customers in Japan, Australia, North America, Europe, and Taiwan, to name a few. We believe we can weather the highs and lows of economic cycle as our FaaS model is resilient as the global trend of going cashless will continue to grow unabated, albeit potentially slower during downturns. What’s more is that our solutions – Fasstap and white label e-wallet solutions – are targeted at budget-conscious businesses and low-cost payment acceptance and will be appealing during downturns.

Besides this, our business model means our direct customer base are mostly FIs, large corporates and global acquirers, which are more resilient to sustain any potential shocks. As our biggest cost component is in human capital, we aren’t immediately impacted from rising inflation as opposed to industries that have direct correlation to cost of raw materials.

5. How are you managing your cash burn while growing market share?

Our objective since our inception has always been to balance growth with profitability by having a sustainable business structure and not to grow through cash burn. This sustainability is anchored on a revenue model that can provide stable recurring revenue flow and that supports annual operating expenses and general capital expenditure. We are unlike an e-commerce or e-marketplace businesses, which is usually a “winner takes all” game and very sensitive to consumer trends and preferences. Instead as a software company, we have the advantage of being able to scale swiftly without having to rely on large economy of scale. This helps us utilise our capital more efficiently.

Having a sustainable and predictable revenue also means that we can meet our expenses efficiently, which include our human capital costs. We believe we can manage our cash effectively and that our customer base will contribute to our revenue for the next 10 years. These customers provide a stable revenue that will make our company become more resilient and we believe this model will weather any possible economic downturn.

As for our growth, we plan to do business with more FIs and large corporate enterprises by leveraging our international partners that include JCB, IDEMIA, and UnionPay International.

6. Do you foresee it being harder for start-ups to raise fund within the next year or so?

We believe it will be more challenging to raise funds given the rising interest rate and the impending potential economic downturn, which makes it difficult for start-ups to attain lofty valuations in the near to middle term. That said, we do believe that any start-ups with strong compelling product and plan, coupled with solid team, will still be able to meet the high demands of investors that still have capital to deploy.

7. Do you have any tips for start-ups who are planning to fundraise?

Those planning to fundraise must first know your company identity. For example, if you are a consumer-facing business, there’ll be different investors from business-facing ones. In our experience, a business-facing type of company has different metrics to consumer-facing businesses. So, knowing your audience is essential as not all venture capitalists – be it financial or strategic investors – may be familiar with the kind of business you’re in.

As long as you have a niche and great product, coupled with knowing what kind of company you are, you will be able to identify the right investor pool, which can come from anywhere around the world and not just from the region you operate in.

8. Where do you see Soft Space in the next 5 years?

The worldwide trend today is for enterprises to focus on innovation in a quest to diversify away from their core capabilities. For example, enterprises who are not traditionally in the finance business are embracing embedded finance, the seamless integration of financial services adopted by non-banks. Success for these “neo-banks” require strong product fundamentals and we are in a position to support such businesses with our technology and expertise.

With this trend booming, the next five years for us is about growth on a global scale and we believe we are poised to achieve this ambition as we are already assimilating our core product offerings with technologies such as Web 3.0 which includes blockchain and Central Bank Digital Currency (CBDC), the digital form of a country’s fiat currency. We also want to grow our FaaS platform and become a key provider to companies and ecosystems that want to embed financial services in their offerings like players such as Stripe, Rapyd, and Adyen. We believe the growing need for convenience and efficient financial services will fuel the growth of this entire embedded finance model.

| DISCLOSURES AND DISCLAIMER |

This Newsletter is strictly informational and is issued Penjana Kapital Sdn Bhd (“PKSB”) on the basis that it is only for the information of the particular person to whom it was provided. This document may not be copied, reproduced, distributed or published by any recipient for any purpose unless Penjana Kapital Sdn Bhd’s prior written consent is obtained. This newsletter has been prepared for information purposes only and is not intended as an offer to sell or a solicitation to buy any securities, and/or any other product in Public or Private markets. Penjana Kapital Sdn Bhd is not making any recommendation to buy any securities or other product and the information provided should not be taken as investment advice.

It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Penjana Kapital Sdn Bhd has no obligation to update its opinion or the information in this newsletter and Penjana Kapital Sdn Bhd recommends that you independently evaluate particular investments and strategies and seek the advice of a financial adviser prior to entering into any transaction. The appropriateness of a particular investment or strategy will depend on your individual circumstances and objectives. The information herein was obtained or derived from sources that Penjana Kapital Sdn Bhd believes are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. All opinions and estimates included in this newsletter constitute our views as of this date and are subject to change without notice.

Penjana Kapital Sdn Bhd is not acting as your advisor and does not owe any fiduciary duties to you in connection with this newsletter and no reliance may be placed on Penjana Kapital Sdn Bhd for advice or recommendations of any sort. Nothing in this newsletter shall constitute legal, accounting or tax advice, or a representation that any transaction or investment is appropriate for you taking into account your investment objectives, financial situation and particular needs, or otherwise constitutes any such advice to you. Penjana Kapital Sdn Bhd makes no representations or warranties, express or implied, with respect to the accuracy of the information or fitness for any particular purpose and does not accept any liability (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) for any use you or your advisors make of the contents of this newsletter or for any loss that may arise from the use of this newsletter or reliance by any person upon such information or opinions provided in the newsletter. This newsletter has been prepared by the analysts of Penjana Kapital Sdn Bhd. Facts and views presented in this newsletter may not reflect the views of or information known to other business units within Penjana Kapital Sdn Bhd. This information herein is not intended to constitute “research” as it is defined by applicable laws. This newsletter is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information provided in this document has been obtained or derived from sources believed to be reliable. Penjana Kapital Sdn Bhd does not guarantee its accuracy or completeness and does not assume any liability for any loss that may result from the reliance by any person upon any such information or opinion. Such information or opinions are subject to change without notice, are for general information only and is not intended as an offer to sell or a recommendation/ solicitation to buy any securities, foreign exchange or other product.